Asset Location Planning

A plan for reducing taxes when it matters most

Asset location planning may help you save on taxes when it matters most, so you can do more of what you love!

Are you looking to increase your tax efficiency while also reducing your tax liability risk. Asset location planning (ALP) is a planning process designed to determine the appropriate tax location for each of your assets so you can potentially reduce taxes when it matters most – during the accumulation, distribution, and transfer phases of your life.

How it works: when you liquidate or sell an asset, there are three ways in which that asset could be taxed: as capital gains, ordinary income, or tax free. Your personalized asset location plan will help determine the correct percentage to invest in each location, which will help position you favorably to pay less taxes as you accumulate, distribute, and transfer your assets.

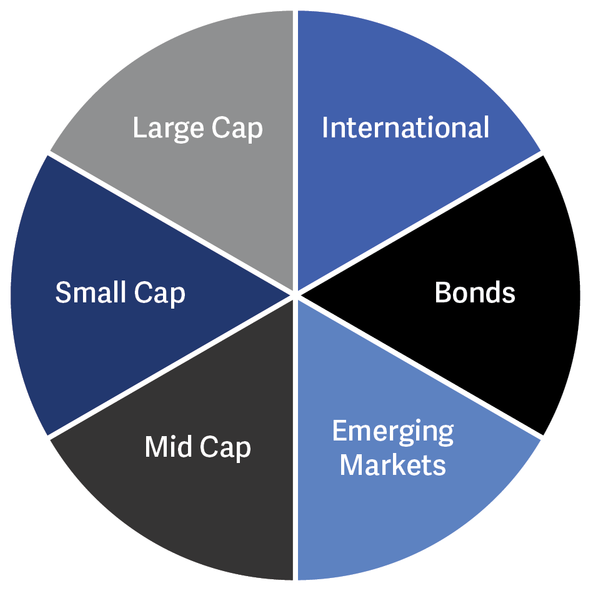

Allocation

Asset allocation is investing in different asset classes to reduce your investment risk.

Asset allocation is the combination of asset classes in your portfolio, such as stocks, bonds, and cash.

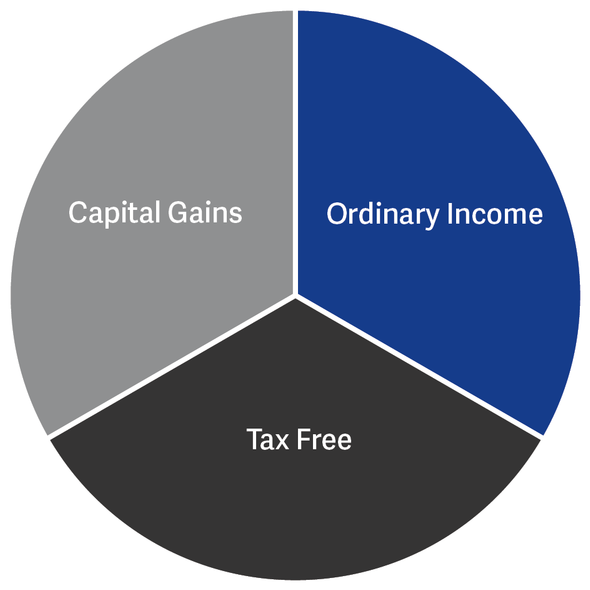

Location

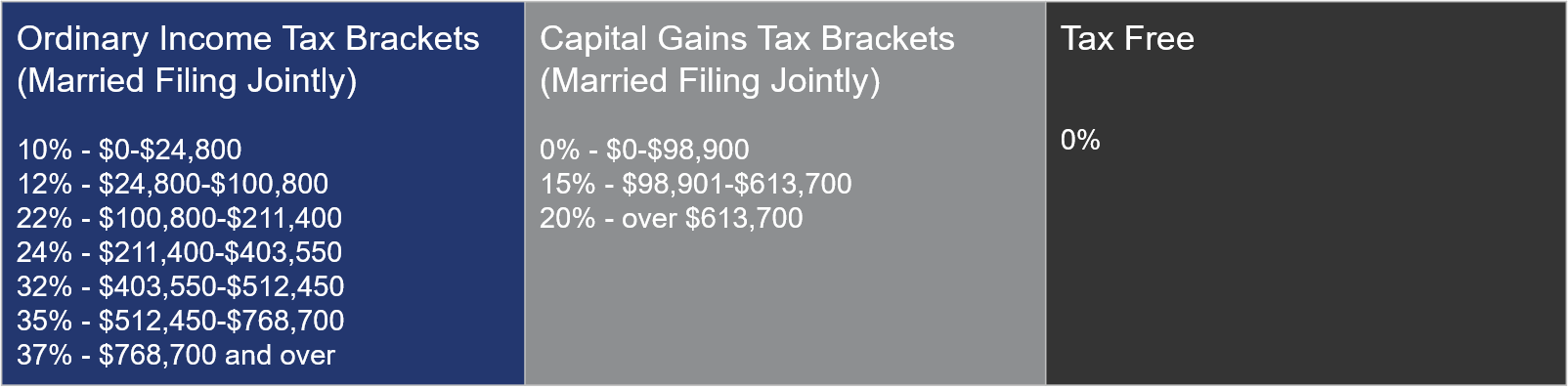

Asset location is investing in different tax locations to reduce your tax liability risk.

Asset location refers to the way your asset will be taxed upon distribution. The three locations are: capital gains, ordinary income, and tax free.

Tax Favored Benefits

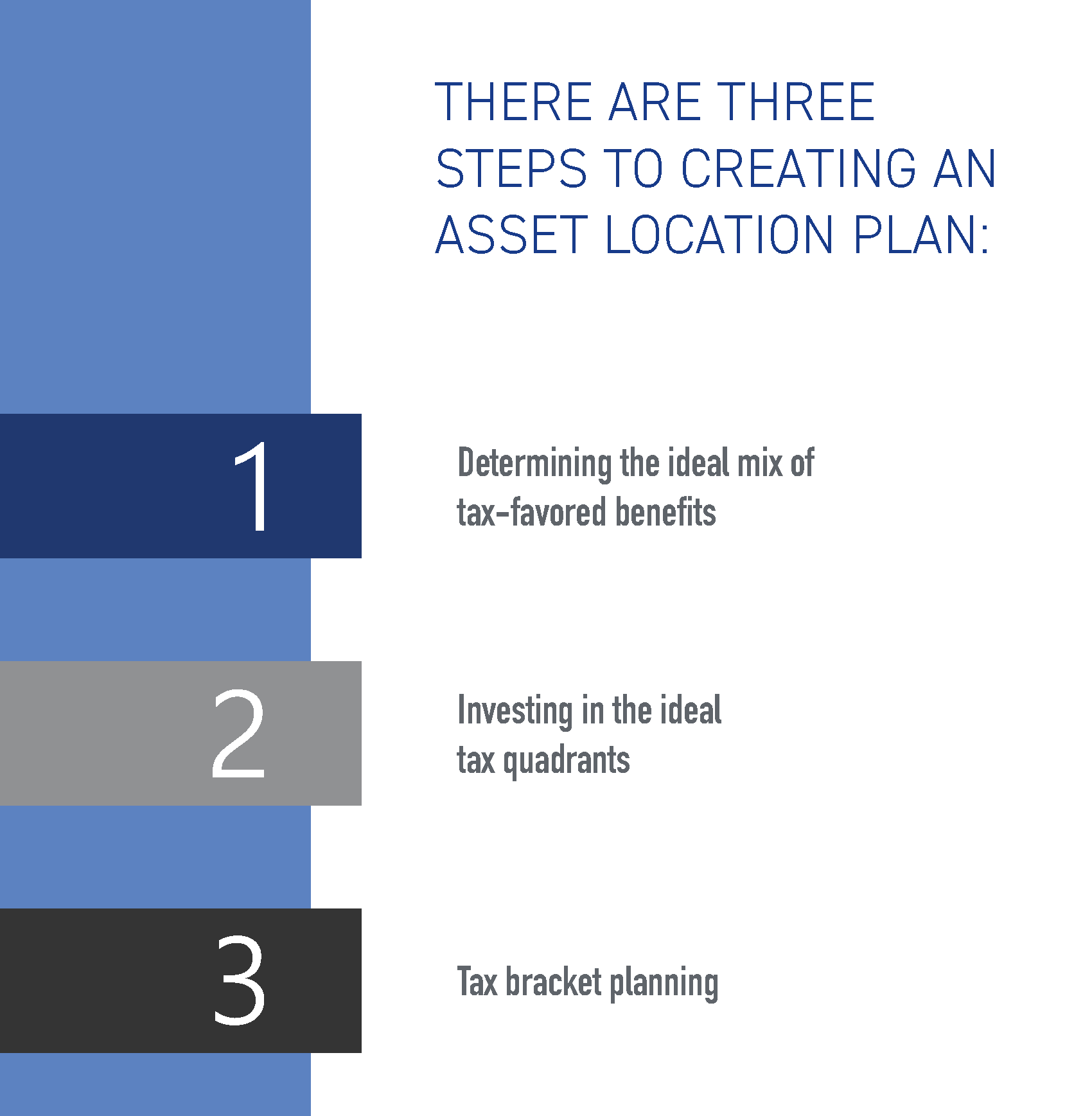

The first step in the asset location planning process is to determine the ideal mix of tax-favored benefits for each of your investments.

The IRS provides three different tax favored benefits – tax deduction on contribution, tax deferral on growth, and tax-free income on distribution. Unfortunately, you can’t get all three benefits within one investment (you have to pay taxes somewhere!), but you can invest in two of the three. Your personalized asset location plan will help determine this mix.

4 Tax Quadrants

Once your ideal mix of tax-favored benefits has been decided, we will determine the optimal amount to invest into each location. There are three phases to every investment: contribution, accumulation, and distribution. The 4 quadrants determine how assets are taxed at each phase of the investment.

Tax Bracket Planning

After your ideal benefits are determined, and a plan for contribution within the different quadrants has been established, the third and final step to your asset location plan will be to calculate the tax impact of your distribution. We call this tax bracket planning – a strategy we employ to get our clients to think about the tax impact of their distributions down the road while keeping the progressive tax system in mind. Tax bracket planning helps you to evaluate which investment location to withdraw from in efforts to minimize the taxes you pay.

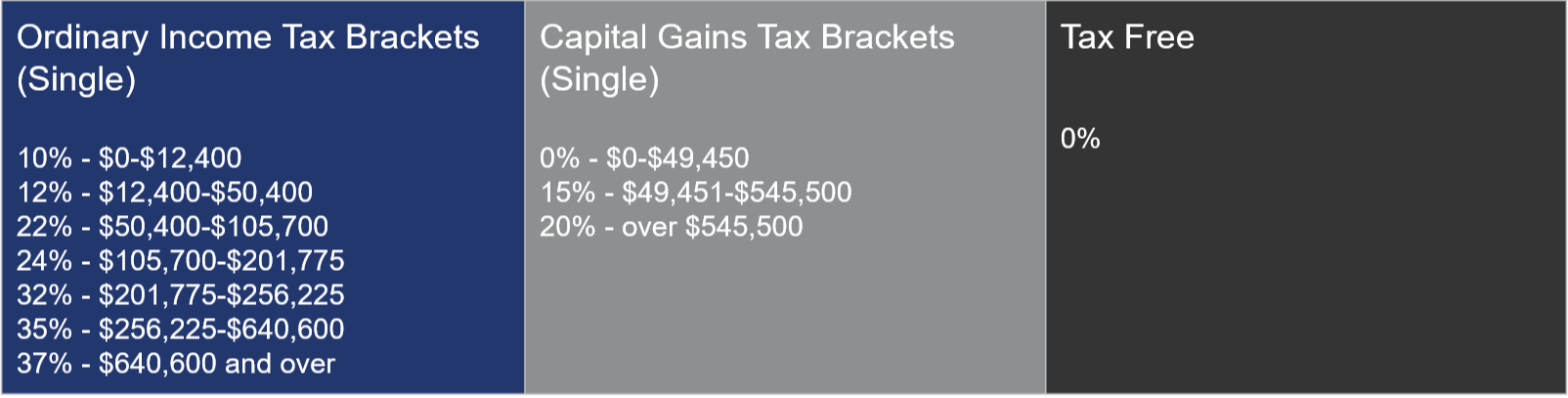

Your total income will be taxed based on the location that your withdrawals come from, for example: if your ordinary income for the year is $350,000, you will be taxed 10% on the first $24,800, 12% on your income from $24,800-$100,800, 22% on your income within the next bracket, and so on (2026 tax brackets for each location reflected here)

Why you may need an Asset Location Plan

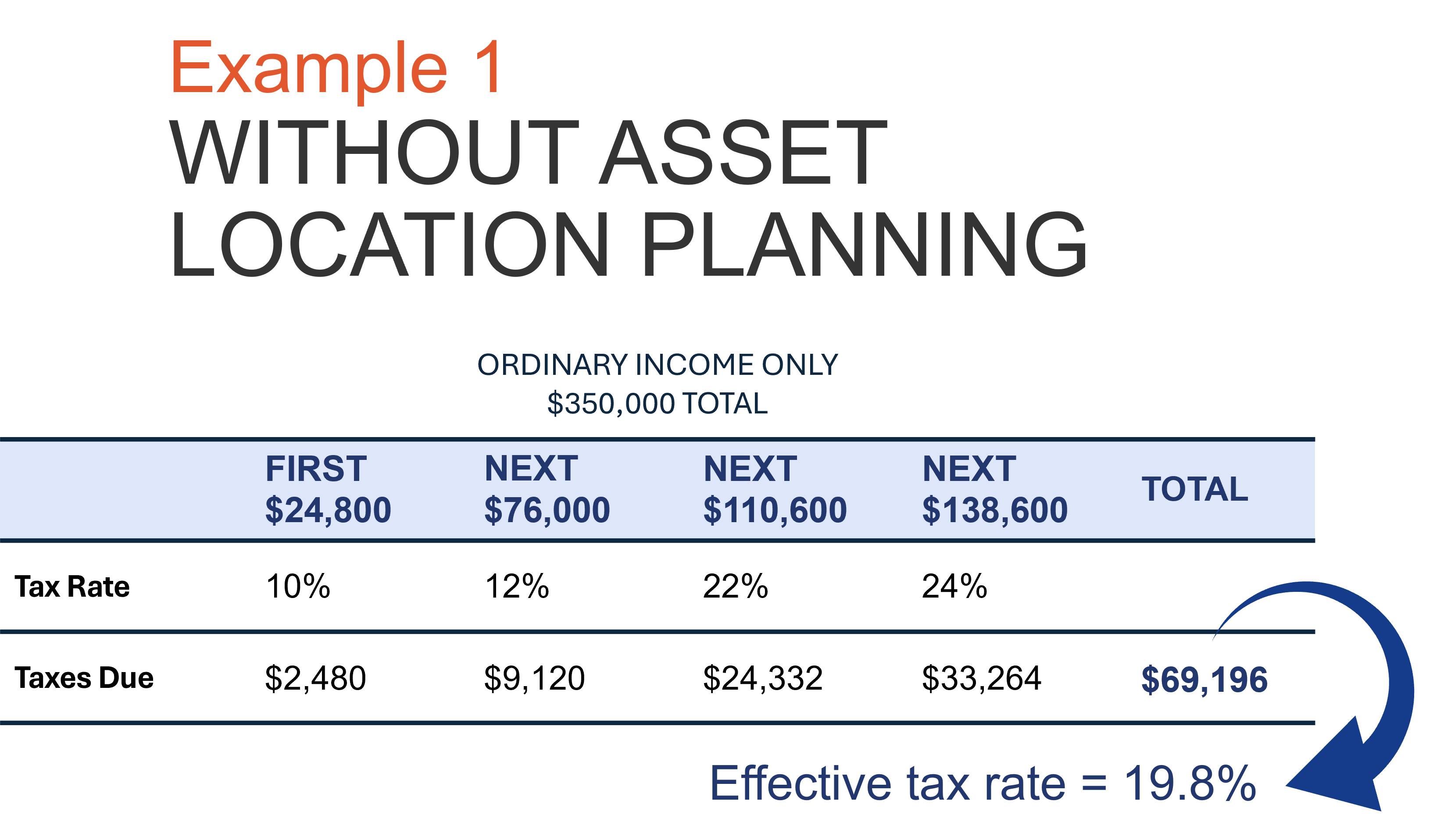

Now that we have a better understanding of tax brackets, let’s take a look at an example using Ivan and Andrea Smith. The Smiths recently retired and will need to withdraw $350,000 for the year from their investments in order to maintain their current lifestyle.

If the Smiths had never put together an asset location plan, they may not have been investing in all three tax locations during their working years, which would mean they may only have the ability to pull their retirement income from one location: the ordinary income location. In this case, they would end up paying $69,196 in taxes, based on current tax treatment.

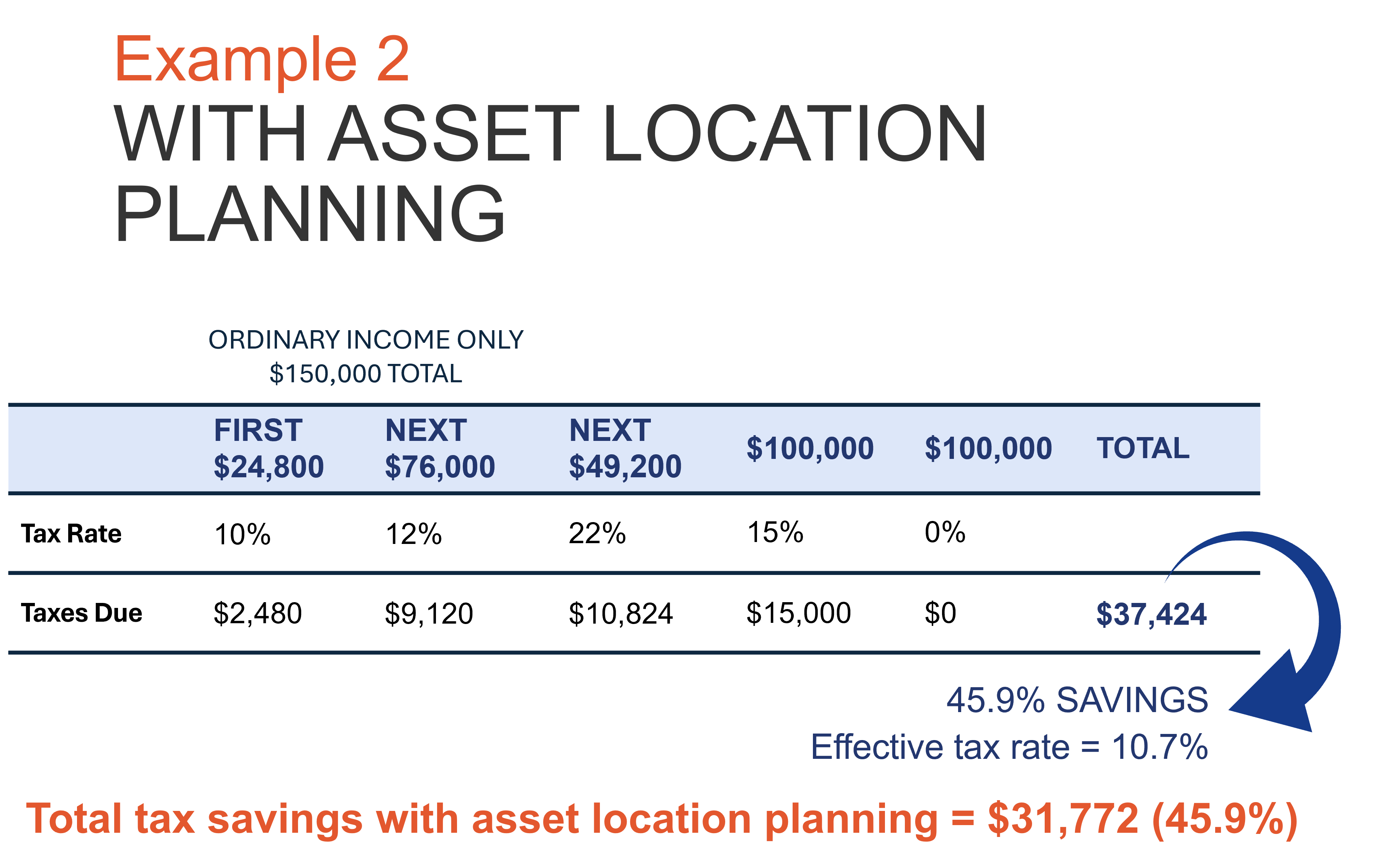

In example 2, the Smiths met with a financial professional and, based on their asset location plan, determined an optimal mix of investment locations. Since they had been investing in all three tax locations, they now have the option to withdraw their $350,000 from each of the three locations. In this case, they can take $150,000 from the ordinary income location, $100,000 from the capital gains location, and $100,000 from the tax-free location.

By determining their tax benefits, finding the ideal tax locations, and tax bracket planning, Ivan and Andrea were able to reduce their effective tax rate from 19.8% to 10.7%, amounting to a savings of $31,772 (45.9%). This gives them the opportunity to spend more on what they love – their grandkids, travel and adventure, golf, and anything else!

While this is just a hypothetical example, with your personalized asset location plan, you can determine how best to potentially reduce your taxes based on your income and objectives.